WHILE OPERATION HOPE CLIENTS FEEL THE ECONOMIC STRUGGLE, FINANCIAL LITERACY INTERVENTIONS DEMONSTRATE SUCCESS

Economic optimism remains low, with only a quarter expressing a positive outlook and half reporting being able to handle a $400 financial emergency

Here are five key findings:

1. Optimism in the U.S. Economy is very low

Only one in four respondents feels optimistic about the economy so far in 2026 (23%). This directly mirrors Gallup’s national data from March, in which only 23% have a positive sentiment about the economy. With so much uncertainty, half say they are concerned or usure about how the economy will affect their financial future over the next year (52%).

2. Clients still feel the cost-of-living crunch from last year

Over half say debt and the high cost of living are the biggest financial challenges they are facing right now (29% and 23%, respectively). Of the different types of debt, credit cards remain the most burdensome at 34%, with student loans (15%), mortgages (14%), and auto loans (11%) trailing behind.

The cost of everyday goods stood out as the factor that most impacted their lives in the first quarter, at 39%, compared to general rising debt levels (25%), housing costs (16%), and work/job dissatisfaction (13%).

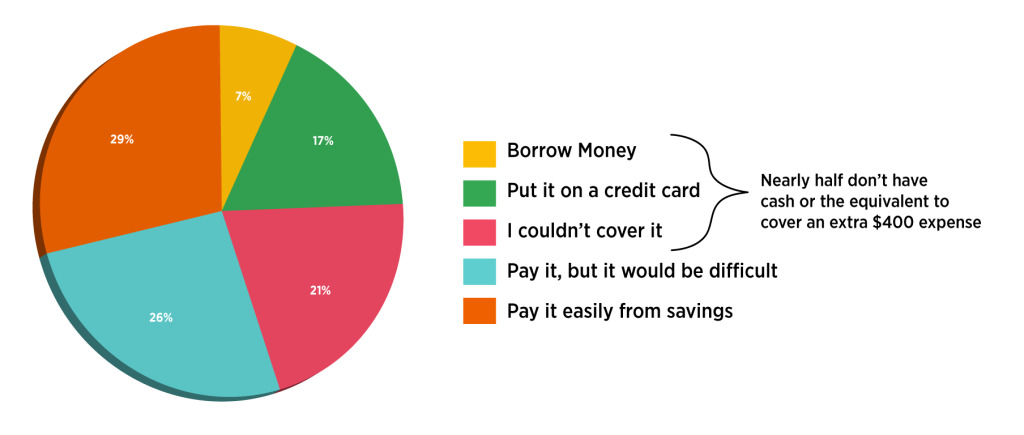

3. Nearly half cannot afford an unexpected expense

73% say they are living paycheck to paycheck, which prevents individuals and families from building an emergency savings. This is demonstrated by how they would handle an unexpected expense: 45% don’t have access to an extra $400 and would have to borrow it, use a credit card, or simply wouldn’t be able to cover it.

If you faced a $400 unexpected expense today, how would you handle it?

4. Our clients demonstrate increased financial resilience versus the average American

Despite a majority living paycheck to paycheck, that amount has actually decreased from last quarter by seven points, from 80% to 73%. Although the remainder of the year will provide a clearer picture, this decline might be attributed to the guidance and education provided by Operation HOPE. As an example, nearly three in four respondents say they feel proactive and informed and are addressing financial decisions despite feeling overwhelmed by the situation (74%). This is in sharp contrast to a February study of 2,000 adults by Experian stating that one-in-five are only slightly confident or not at all confident understanding their personal finances.

5. More respondents are doing better financially than last quarter

38% say they are better off financially than they were a year ago. This is a significant increase from those who gave the same answer last quarter, at 27%. Additionally, those who say their personal debt levels increased over the last three months declined quarter-over-quarter, from 55% to 45%. This has led to a five-point increase in hopefulness of their financial wellbeing over the next year, at 81%.

in the news